Note

You can download this demonstration as a Jupyter Notebook

here

Wealth transfer

This notebook presents a tutorial for beginners on how to create a simple agent-based model with the agentpy package. It demonstrates how to create a basic model with a custom agent type, run a simulation, record data, and visualize results.

[1]:

# Model design

import agentpy as ap

import numpy as np

# Visualization

import seaborn as sns

About the model

The model explores the distribution of wealth under a trading population of agents. Each agent starts with one unit of wealth. During each time-step, each agents with positive wealth randomly selects a trading partner and gives them one unit of their wealth. We will see that this random interaction will create an inequality of wealth that follows a Boltzmann distribution. The original version of this model been written in MESA and can be found here.

Model definition

We start by defining a new type of Agent with the following methods:

setup()is called automatically when a new agent is created and initializes a variablewealth.wealth_transfer()describes the agent’s behavior at every time-step and will be called by the model.

[2]:

class WealthAgent(ap.Agent):

""" An agent with wealth """

def setup(self):

self.wealth = 1

def wealth_transfer(self):

if self.wealth > 0:

partner = self.model.agents.random()

partner.wealth += 1

self.wealth -= 1

Next, we define a method to calculate the Gini Coefficient, which will measure the inequality among our agents.

[3]:

def gini(x):

""" Calculate Gini Coefficient """

# By Warren Weckesser https://stackoverflow.com/a/39513799

x = np.array(x)

mad = np.abs(np.subtract.outer(x, x)).mean() # Mean absolute difference

rmad = mad / np.mean(x) # Relative mean absolute difference

return 0.5 * rmad

Finally, we define our `Model <https://agentpy.readthedocs.io/en/stable/reference_models.html>`__ with the following methods:

setupdefines how many agents should be created at the beginning of the simulation.stepcalls all agents during each time-step to perform theirwealth_transfermethod.updatecalculates and record the current Gini coefficient after each time-step.end, which is called at the end of the simulation, we record the wealth of each agent.

[4]:

class WealthModel(ap.Model):

""" A simple model of random wealth transfers """

def setup(self):

self.agents = ap.AgentList(self, self.p.agents, WealthAgent)

def step(self):

self.agents.wealth_transfer()

def update(self):

self.record('Gini Coefficient', gini(self.agents.wealth))

def end(self):

self.agents.record('wealth')

Simulation run

To prepare, we define parameter dictionary with a random seed, the number of agents, and the number of time-steps.

[5]:

parameters = {

'agents': 100,

'steps': 100,

'seed': 42,

}

To perform a simulation, we initialize our model with a given set of parameters and call `Model.run() <https://agentpy.readthedocs.io/en/stable/reference_models.html>`__.

[6]:

model = WealthModel(parameters)

results = model.run()

Completed: 100 steps

Run time: 0:00:00.124199

Simulation finished

Output analysis

The simulation returns a `DataDict <https://agentpy.readthedocs.io/en/stable/reference_output.html>`__ with our recorded variables.

[7]:

results

[7]:

DataDict {

'info': Dictionary with 9 keys

'parameters':

'constants': Dictionary with 3 keys

'variables':

'WealthModel': DataFrame with 1 variable and 101 rows

'WealthAgent': DataFrame with 1 variable and 100 rows

}

The output’s info provides general information about the simulation.

[8]:

results.info

[8]:

{'model_type': 'WealthModel',

'time_stamp': '2021-05-28 09:33:50',

'agentpy_version': '0.0.8.dev0',

'python_version': '3.8.5',

'experiment': False,

'completed': True,

'created_objects': 100,

'completed_steps': 100,

'run_time': '0:00:00.124199'}

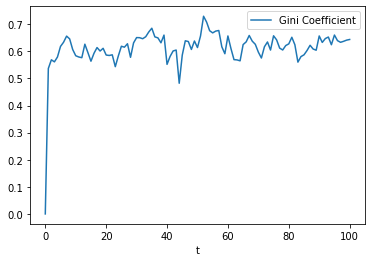

To explore the evolution of inequality, we look at the recorded `DataFrame <https://pandas.pydata.org/pandas-docs/stable/reference/api/pandas.DataFrame.html>`__ of the model’s variables.

[9]:

results.variables.WealthModel.head()

[9]:

| Gini Coefficient | |

|---|---|

| t | |

| 0 | 0.0000 |

| 1 | 0.5370 |

| 2 | 0.5690 |

| 3 | 0.5614 |

| 4 | 0.5794 |

To visualize this data, we can use `DataFrame.plot <https://pandas.pydata.org/pandas-docs/stable/reference/api/pandas.DataFrame.plot.html>`__.

[10]:

data = results.variables.WealthModel

ax = data.plot()

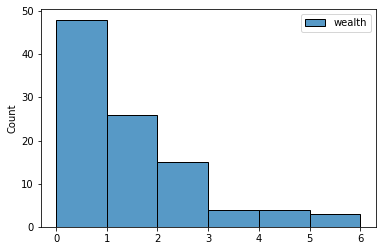

To look at the distribution at the end of the simulation, we visualize the recorded agent variables with seaborn.

[11]:

sns.histplot(data=results.variables.WealthAgent, binwidth=1);

The result resembles a Boltzmann distribution.